Closing Entries in Accounting: Everything You Need to Know +How to Post Them

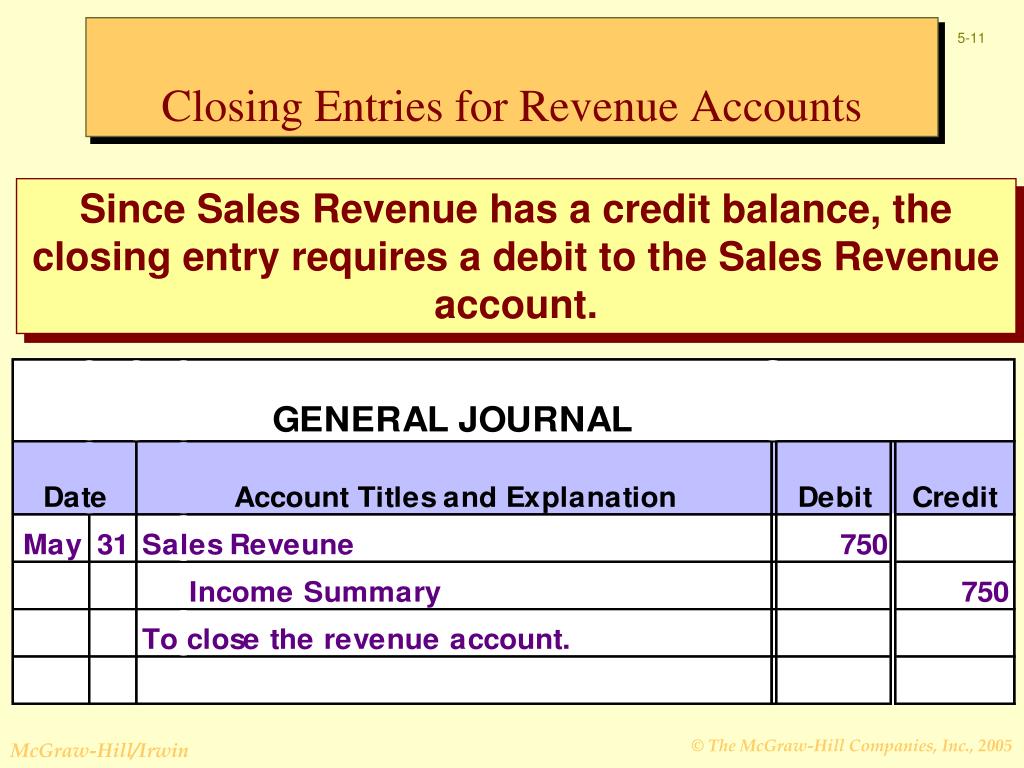

There is no need to close temporary accounts to another temporary account (income summary account) in order to then close that again. We see from the adjusted trial balance that our revenue account has a credit balance. To make the balance zero, debit the revenue account and credit the Income Summary account. Other accounting software, such as Oracle’s PeopleSoft™, post closing entries to a special accounting period that keeps them separate from all of the other entries.

What Is Net Income?

However, if the company also wanted to keep year-to-dateinformation from month to month, a separate set of records could bekept as the company progresses through the remaining months in theyear. For our purposes, assume that we are closing the books at theend of each month unless otherwise noted. “The books” are a company’s record of financial transactions. The records are used to generate reports that tell an owner how much money flows in and out of their business.

- If this is the case, then this temporary dividends account needs to be closed at the end of the period to the capital account, Retained Earnings.

- What did we do with net income when preparing the financial statements?

- In addition, if the accounting system uses subledgers, it must close out each subledger for the month prior to closing the general ledger for the entire company.

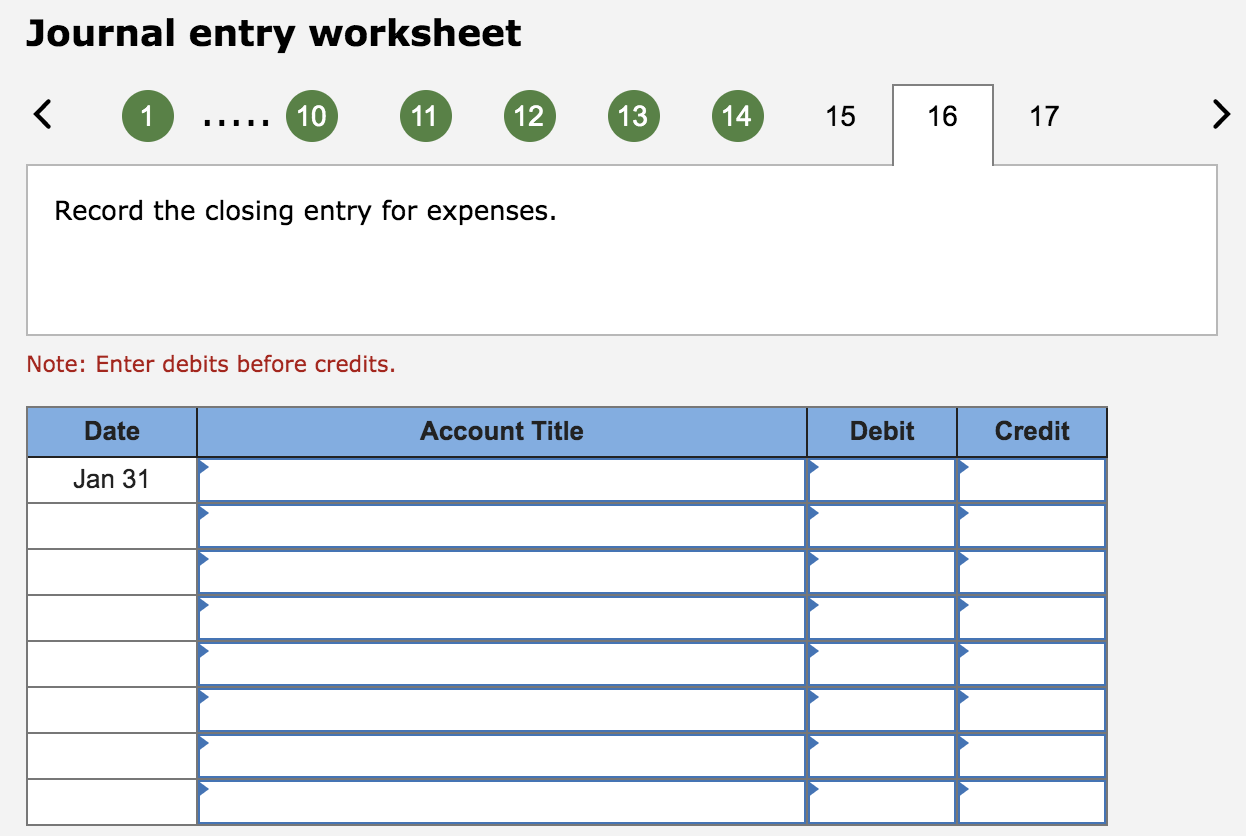

- Temporary accounts include all revenue and expense accounts, and also withdrawal accounts of owner/s in the case of sole proprietorships and partnerships (dividends for corporations).

- This crucial step ensures that financial records are accurate and up-to-date for the next period, making it easier to track the company’s performance over time.

Trial Balance

You might be asking yourself, “is the Income Summary accounteven necessary? ” Could we just close out revenues and expensesdirectly into retained earnings and not have this extra temporaryaccount? We could do this, but by having the Income Summaryaccount, you get a balance for net income a second time.

Permanent Versus Temporary Accounts

In 2006, she obtained her MS in Accounting and Taxation and was diagnosed with Hodgkin’s Lymphoma two months later. Instead of focusing on the fear and anger, she started her accounting and consulting firm. In the last 10 years, she has worked with clients all over the country and now sees her diagnosis as an opportunity that opened doors to a fulfilling life. Kristin is also the creator of Accounting In Focus, a website for students taking accounting courses.

Retained earnings are those earnings not distributed to shareholders as dividends, but retained for further investment, often in advertising, sales, production, and equipment. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. Our T-account for Retained Earnings now has the desired balance. The balance in Retained Earnings was $8,200 before completing the Statement of Retained Earnings.

What is the purpose of the Income Summary account?

This gives you a preliminary ending balance for each account. Free accounting templates can help you keep your journal entries in order and manage your bookkeeping in a straightforward manner. Closing entries are crucial for maintaining accurate financial records. HighRadius has a comprehensive Record to Report suite that revolutionizes your accounting processes, making them more efficient and accurate.

The trial balance, after the closing entries are completed, is now ready for the new year to begin. Think back to all the journal entries you’ve completed so far. If you have only done journal entries and adjusting journal entries, the answer is no. Let’s look at the trial balance we used in the Creating Financial Statements post. The income statementsummarizes your income, as does income summary.

Whenyou compare the retained earnings ledger (T-account) to thestatement of retained earnings, the figures must match. It isimportant to understand retained earnings is not closed out, it is only updated. RetainedEarnings is the only account that appears in the closing entriesthat does not close. You should recall from your previous materialthat retained why use accounting software earnings are the earnings retained by the companyover time—not cash flow but earnings. Now that we have closed thetemporary accounts, let’s review what the post-closing ledger(T-accounts) looks like for Printing Plus. Closing entries are posted in the general ledger by transferring all revenue and expense account balances to the income summary account.

If the account has a $90,000 credit balance and we wanted to bring the balance to zero, what do we need to do to that account? In order to cancel out the credit balance, we would need to debit the account. “The books” are a business’s revenue, expense, and income summary reports. Business owners can close their books by zeroing out their income and expense accounts and then plugging net profit (or loss) into the balance sheet. At the end of the year, all the temporary accounts must be closed or reset, so the beginning of the following year will have a clean balance to start with. In other words, revenue, expense, and withdrawal accounts always have a zero balance at the start of the year because they are always closed at the end of the previous year.

Leave a reply →